One of the Affordable Care Act (ACA)’s goals was to help people purchase affordable private health plans by subsidizing premiums and cost sharing for eligible households. Yet many individual market enrollees still report cost as a barrier to care and are displeased with the health care system. While the individual market exchanges, like Connect for Health Colorado, were supposed to be a pillar of the ACA and were expected to increase enrollment, individual market enrollment has remained steady over the past decade in Colorado, likely due to ongoing and unresolved access to care and cost barriers.

Image

2023 CHAS: Individual Market

Individual Market Enrollees Faced Higher Barriers to Care

January 8, 2025

January 9, 2026

Important note: Data from the 2021 and 2023 Colorado Health Access Surveys have been revised to reflect a slight change in data weighting. Certain materials, including data briefs like this one, have not been updated. For the most current data, visit the 2025 CHAS page. Learn more about the weighting change.

During the open enrollment period each year, about 300,000 Coloradans with individual market insurance must decide which plan best suits their family’s needs and their pocketbook.

Findings

The Health Care System Was Not Meeting Many Individual Market Enrollees’ Needs.

The Colorado Health Access Survey (CHAS) data found that individual market enrollees were more likely than Coloradans with other health care coverage to report that the health care system was not meeting their family’s needs. One in four people with individual market health care coverage (27.1%) disagreed or strongly disagreed that the health care system was meeting the needs of their family, compared with 15.6% of Coloradans with employer-sponsored insurance (ESI), 5.6% with Medicare, and 14.6% enrolled in Medicaid or Child Health Plan Plus (CHP+).

Data from the CHAS points to three factors that may have contributed to this overall dissatisfaction among individual market enrollees.

Factor 1. Accessing Needed Care Is a Growing Challenge

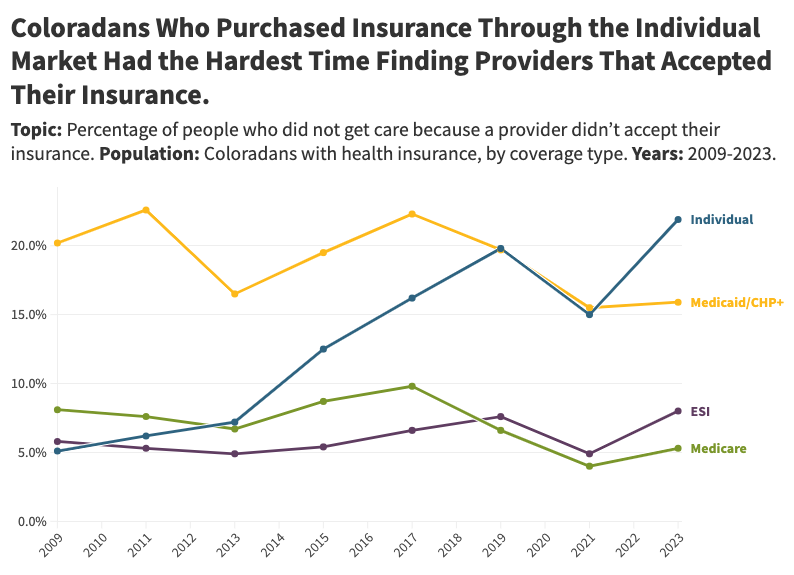

Individual market enrollees had a harder time finding doctors that accepted their insurance in 2023 compared to those with other coverage options. Over one in five enrollees (21.9%) struggled to find a doctor that accepted their insurance, compared to Coloradans with employer-sponsored insurance (8.0%), Medicare (5.3%), and Medicaid/CHP+ (15.9%).

Finding a doctor to accept their insurance has become even harder for individual market enrollees over time. Enrollees were over three times more likely to report having this issue in 2023 (21.9%), compared with 2013 (7.2%). This growing challenge was also unique to individual market enrollees. Coloradans covered by other insurance types, such as employer-sponsored insurance, Medicare, and Medicaid/CHP+, did not see such a steady increase in providers not accepting their insurance between 2009 and 2023. Individual market enrollees might have had fewer provider options because insurers sometimes limit provider networks to reduce plan costs.

{kind=link}

Factor 2. Health Care Remained Expensive for Individual Market Enrollees

Across insurance types, Coloradans reported the cost of needed care and prescription medications as a barrier, but individual market enrollees reported cost as a barrier to care more than people with other insurance coverage. While many individual market enrollees have access to premium tax credits (financial assistance that lowers the monthly cost of health insurance for individuals and families), insurance plans often have high deductibles, which must be fully paid out of pocket before insurance begins covering care costs. However, once deductibles have been met, some people still need to pay coinsurance, a requirement that enrollees pay a percentage of their total cost of care.

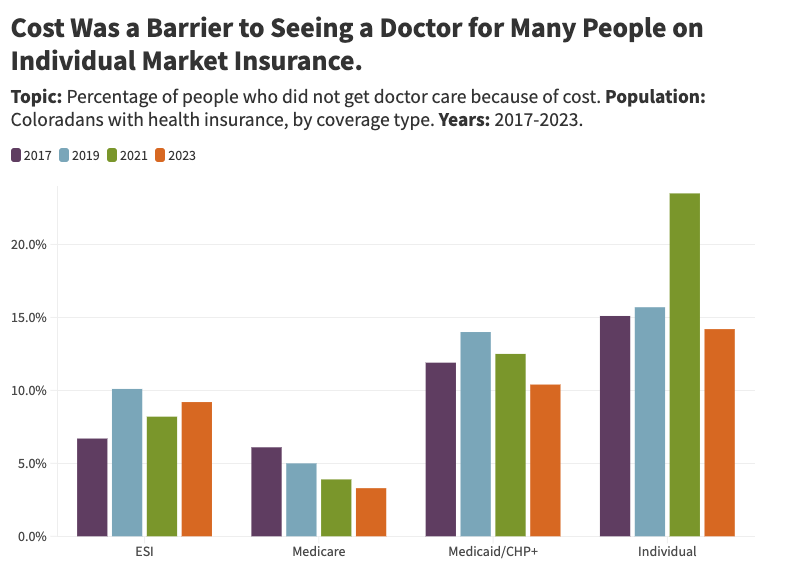

Doctor Care. About one in seven Coloradans (14.2%) on the individual market didn’t get needed care from a doctor because of cost, compared with 9.2% with employer-sponsored insurance, 3.3% with Medicare, and 10.4% with Medicaid/CHP+. Rates of people not seeing the doctor because of cost for individual market enrollees have remained higher than other coverage options since 2017.

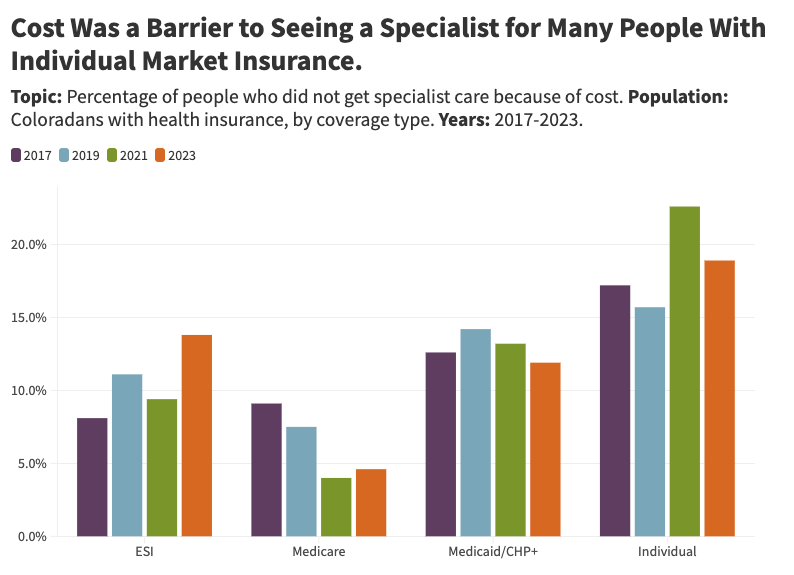

Specialist Care. Almost one in five people (18.9%) on the individual market who needed specialist care did not get it because of cost. This rate is higher than for other coverage types: employer-sponsored insurance (13.8%), Medicare (4.6%), and Medicaid/CHP+ (11.9%). Individual market enrollees have had the most trouble accessing specialist care because of cost since 2017.

Dental Care. More than one in five Coloradans (22.4%) on the individual market did not get needed dental care because of cost. Medicaid/CHP+ and individual market enrollees reported cost as a barrier at a rate almost twice that of Coloradans with Medicare or employer-sponsored insurance.

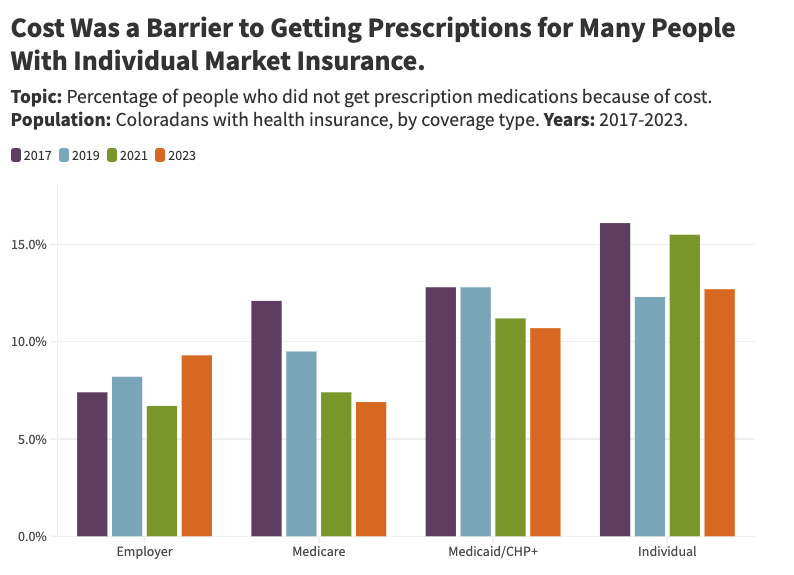

Prescription Medications. Affording prescription medications was more challenging for individual market enrollees compared to Coloradans with other coverage types in 2023. The percentage of those challenged with affording prescription medications has fluctuated since 2017, with either Medicaid or individual market enrollees reporting the highest rates.

Factor 3. Higher Rates of Churn and Coverage Instability

Individual market enrollees were more likely to change coverage during the year — an occurrence known as churn — or to have unstable coverage in 2023. Churn can occur because people leave their jobs, have changes in their public coverage eligibility, or have a life-changing event. Insurance disruptions and instability can increase the risk for coverage gaps, delay needed care, and result in poorer health outcomes.

Individual market enrollees were less likely to be insured for all of the past 12 months compared to Coloradans with other coverage:

- Employer sponsored insurance: 83.3%

- Medicare: 90.1%

- Medicaid/CHP+: 89.0%

- Individual: 73.6%.

Additionally, individual market enrollees were more likely than those covered by employer-sponsored insurance and public insurance (Medicare and Medicaid) to have reported losing coverage.

Looking Ahead

The individual market allows Coloradans without employer-sponsored or public insurance options to access health care plans for themselves and their families. While the ACA created more consumer protections and offered financial assistance, which were enhanced by and the Inflation Reduction Act (IRA) and American Rescue Plan Act (ARPA), many individual market enrollees remain dissatisfied with the health care system.

Health care costs, doctor accessibility, and coverage instability were ongoing issues for people who were enrolled in individual market insurance. The Colorado Option waiver, approved in 2022 and implemented in 2023, sought to address this affordability issue by creating standardized plans that would lower premium costs for enrollees. The impact of the waiver is still unclear, especially as the cost of 2025 Colorado Option plans are expected to rise by almost 5%.

As current and prospective individual market enrollees select their health care plans, concerns about cost, accessing care, and coverage stability will likely be top of mind. How the Colorado Option will improve these barriers and what other policies are needed will become more clear with 2025 and 2027 CHAS data.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}